If you've ever tried to build comparison content in the insurance space, you've probably discovered the uncomfortable truth: insurance is different. Unlike banking or investing comparisons, where editorial content has clear safe harbors, insurance comparison content walks a fine line between helpful information and regulated advice.

The challenge stems from state-level regulation. Every state has its own insurance commission with its own rules about who can discuss, recommend, or quote insurance products. What's perfectly legal editorial content in one state might require a producer's license in another. Add in the complexity of different insurance types—life, health, auto, home, commercial—and you've got a regulatory maze.

But here's the opportunity: precisely because insurance content is so complex, there's less competition from quality comparison sites. If you can navigate the regulations correctly, you can build valuable content in a space where most publishers fear to tread.

This guide provides a practical framework for creating insurance comparison content that provides genuine value while staying on the right side of state insurance regulations. We'll cover what you can and can't do without licensing, content patterns that work, and the specific disclosures that protect you.

Understanding the Regulatory Landscape

Before creating any insurance comparison content, you need to understand who regulates this space and what they care about. Getting this wrong can have serious consequences.

Who Regulates Insurance Content?

Unlike securities (regulated by the SEC) or banking (regulated by federal agencies), insurance is primarily regulated at the state level. Each state has its own:

- Insurance commissioner or department: The regulatory body that oversees insurance in that state

- Licensing requirements: Rules about who can sell, solicit, or advise on insurance

- Advertising regulations: Specific rules about how insurance can be marketed

- Disclosure requirements: What must be disclosed when discussing insurance products

The NAIC (National Association of Insurance Commissioners) provides model regulations that many states adopt, but implementation varies significantly. What's compliant in California might not be compliant in Texas.

The Critical Distinction: Editorial vs. Solicitation

The most important concept for insurance content creators is the distinction between editorial content and solicitation. Here's how to think about it:

| Editorial Content (Generally Safe) | Solicitation (Requires Licensing) |

|---|---|

| Explaining how insurance types work | Recommending specific policies to individuals |

| Comparing publicly available features | Providing personalized quotes |

| Discussing general pros/cons of insurers | Helping users apply for coverage |

| Educational content about coverage types | Advising on coverage amounts needed |

| Aggregating public reviews and ratings | Acting as an intermediary in purchase |

The general principle: you can inform and educate, but you typically can't advise, recommend to specific individuals, or facilitate purchases without appropriate licensing.

Insurance Content Types and Risk Levels

Different types of insurance content carry different regulatory risk levels. Understanding this spectrum helps you choose what to create.

Low-Risk Content Patterns

These content types are generally considered editorial and carry lower regulatory risk:

Educational explainers: “What is term life insurance?” or “How does deductible affect your auto insurance premium?” content that explains concepts without recommending specific products is typically safe.

Company profile comparisons: Comparing the publicly available information about insurance companies—financial strength ratings, customer service reputation, claims handling, company history—without recommending specific policies.

Coverage type comparisons: Explaining the differences between term and whole life, or HMO vs PPO health plans, as educational content rather than purchase guidance.

Review aggregation: Collecting and presenting publicly available reviews, ratings, and complaints data without editorializing about which insurer someone should choose.

Medium-Risk Content Patterns

These content types require more careful handling:

“Best” lists with rankings: Creating listicles like “Best Life Insurance Companies” is possible but requires careful framing. The ranking should be based on objective criteria, not personal recommendations.

Price comparisons: Showing average or example pricing is riskier than feature comparisons because it gets closer to quote territory. Using clearly labeled example rates with extensive disclaimers is safer.

Coverage recommendations by category: “Best life insurance for seniors” is riskier than “Life insurance options for seniors” because “best” implies a recommendation.

High-Risk Content Patterns (Avoid Without Licensing)

These content types typically require insurance producer licensing:

- Providing personalized quotes or rate estimates

- Recommending specific coverage amounts (“You need $500K of life insurance”)

- Advising which specific policy someone should buy

- Collecting user information for quote purposes

- Acting as an intermediary between users and insurers

- Receiving commission on policy sales (without licensing)

| Content Type | Risk Level | Key Requirements |

|---|---|---|

| Educational explainers | Low | Clear “not advice” disclaimers |

| Company comparisons | Low-Medium | Objective criteria, source citations |

| “Best of” rankings | Medium | Transparent methodology, general disclaimers |

| Price/rate content | Medium-High | Example rates only, extensive disclaimers |

| Personalized recommendations | High | Producer licensing required |

Safe Content Patterns That Work

Let's look at specific content patterns that provide value while staying in the safe zone.

Pattern 1: Methodology-First Comparisons

Lead with your methodology to establish that rankings are based on objective criteria, not individual advice. This framing helps position your content as editorial analysis rather than recommendations.

This approach works because you're presenting factual analysis based on publicly available data, not personal recommendations about what someone should buy.

Pattern 2: Category Guidance, Not Individual Advice

Instead of telling individuals what to buy, describe what types of products might suit different categories of people. The distinction is subtle but important.

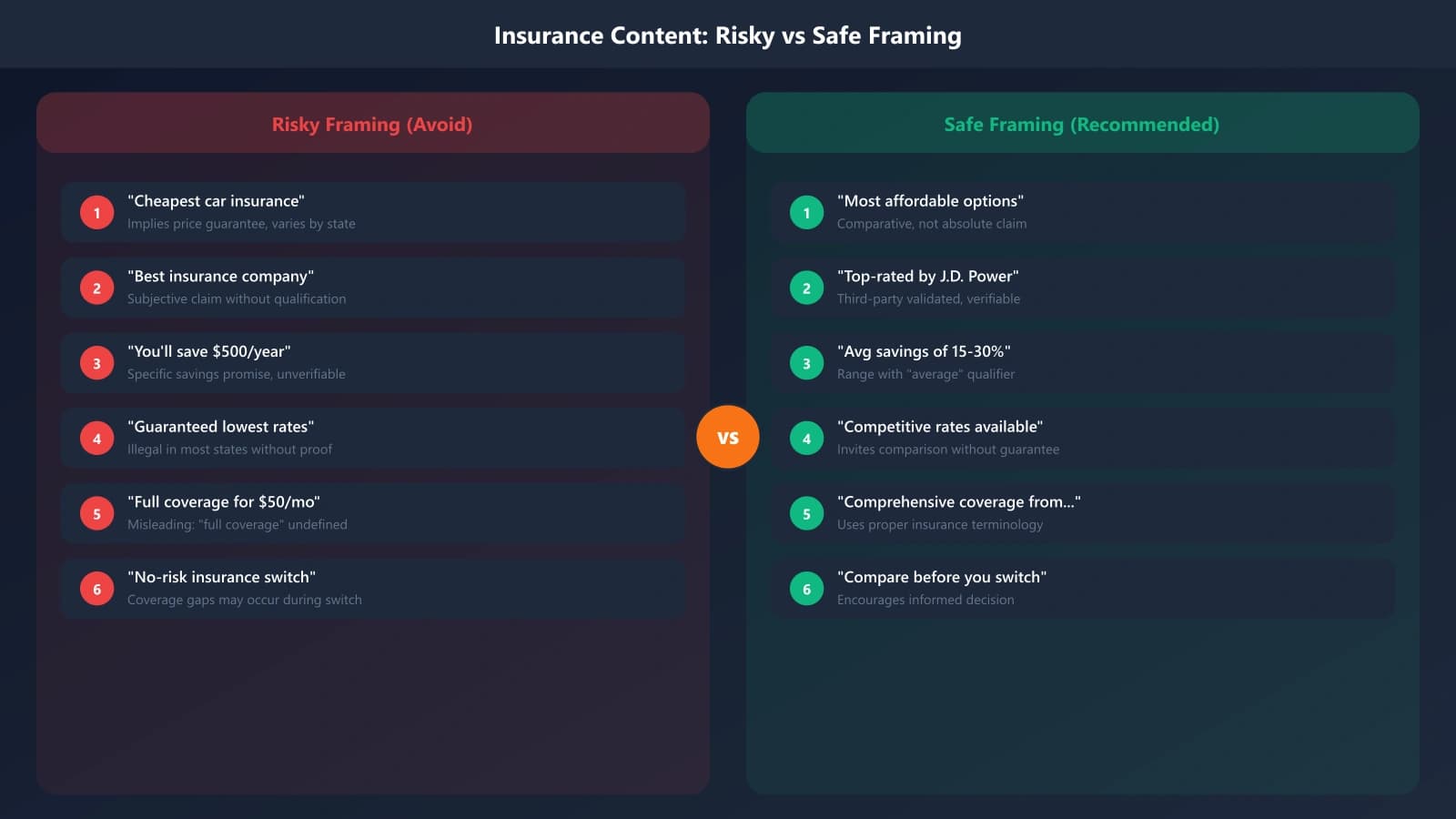

Risky framing: “You should buy term life insurance if you're young and healthy.”

Safer framing: “Term life insurance is often a fit for people in their 20s-40s who want affordable coverage during their peak earning years and have other investment vehicles for long-term wealth building.”

The safer version describes a category of people and product fit without directly advising an individual reader.

Pattern 3: Question-Based Frameworks

Rather than making recommendations, provide frameworks that help readers ask the right questions when shopping for insurance on their own.

Example: “5 Questions to Ask Before Buying Life Insurance”

- What are the insurer's financial strength ratings from AM Best, S&P, and Moody's?

- What is the company's claims-paying history and customer satisfaction score?

- How do the policy features compare to similar products?

- What are the total costs over the policy term, including all fees?

- What is the company's complaint ratio compared to industry average?

This pattern provides value by educating readers on evaluation criteria without making specific recommendations.

Generate Compliant Insurance Comparisons

Create insurance comparison pages with proper disclaimers and regulatory-safe content structures.

Try for FreeRequired Disclosures for Insurance Content

Proper disclosure is your primary protection when creating insurance comparison content. Here are the essential disclosures to include.

Core Disclosures

Every insurance comparison page should include:

Additional Disclosures by Content Type

For price/rate content: “Sample rates shown are for illustrative purposes only based on [specific profile, e.g., 'a 35-year-old non-smoking male in excellent health']. Your actual rates will vary based on your individual profile, location, and other factors. Obtain quotes directly from insurers or licensed agents for accurate pricing.”

For affiliate content: “We may receive compensation when you click links to insurance companies on this page. This compensation does not influence our editorial rankings, which are based on [describe methodology]. We maintain editorial independence from our advertising partners.”

For “best” rankings: “Our 'best' rankings reflect our analysis of publicly available data including financial strength ratings, customer satisfaction surveys, and complaint data. They represent editorial opinion based on general criteria and may not reflect the best choice for your individual circumstances.”

Disclosure Placement

Where you place disclosures matters as much as what they say:

- Page-level disclaimer: A comprehensive disclaimer should appear near the top of any insurance comparison page, before the main content

- Rate disclaimers: Should appear immediately adjacent to any pricing information

- Affiliate disclosures: Should appear before the first link to an insurance company

- Footer disclaimer: A comprehensive site-wide disclaimer in the footer reinforces page-level disclosures

Insurance Type Considerations

Different insurance types have different regulatory sensitivities. Here's what to know for major categories.

Life Insurance

Life insurance comparison is relatively approachable because:

- Product features are fairly standardized (term vs. whole, coverage amounts)

- Financial strength ratings provide objective comparison criteria

- Educational content about life insurance basics is clearly editorial

Key considerations: Avoid coverage amount recommendations (“You need X times your salary”). Stick to feature and company comparisons.

Health Insurance

Health insurance comparison is more complex due to:

- ACA regulations and marketplace complexity

- State-specific plan availability

- Subsidy calculations that affect affordability

Key considerations: Focus on educational content about plan types (HMO/PPO/EPO) and coverage concepts. Avoid personalized recommendations or subsidy calculations without proper licensing.

Auto and Home Insurance

Property and casualty insurance comparisons are common online, but still carry regulatory considerations:

- Rate comparisons require extensive disclaimers about individual variation

- State-specific regulations vary significantly

- Many successful sites in this space are licensed or partner with licensed entities

Key considerations: Company reputation comparisons based on claims handling and customer service are safer than rate comparisons.

| Insurance Type | Content Complexity | Regulatory Sensitivity | Recommended Focus |

|---|---|---|---|

| Life Insurance | Moderate | Moderate | Company reputation, product types |

| Health Insurance | High | High | Educational content, plan type explanations |

| Auto Insurance | Moderate | Moderate-High | Company comparisons, claims reputation |

| Home Insurance | Moderate | Moderate | Coverage education, company reputation |

| Commercial Insurance | High | High | Educational only, partner with licensed brokers |

Monetization Options

Monetizing insurance content without licensing requires creative approaches. Here are legitimate options.

Lead Generation Partnerships

Many licensed insurance aggregators and agencies pay for leads. The key is structuring the relationship correctly:

- You provide educational content and traffic

- Licensed partner handles quote generation and sales

- You receive payment for referrals, not sales (important distinction)

- Clear disclosure that you're referring to a licensed partner

Display Advertising

Insurance advertising CPMs are among the highest for any vertical. Quality insurance comparison content can monetize well through:

- Premium ad networks with finance-focused advertisers

- Direct advertising relationships with insurance companies (for brand awareness, not solicitation)

- Sponsored content with clear disclosure

Affiliate Program Caution

Traditional affiliate relationships in insurance are complex. Many “insurance affiliate programs” actually require licensing or are structured as lead generation. Before joining any program:

- Verify the relationship structure doesn't require licensing

- Understand exactly what action triggers payment

- Consult with an attorney if unclear

Putting It Into Practice

Insurance comparison content is challenging but not impossible. The key is respecting the regulatory boundaries while finding ways to provide genuine value within those constraints.

Here's your implementation checklist:

- Choose your insurance type carefully. Start with categories where educational content clearly fits (life insurance basics, company reputation comparisons).

- Lead with methodology. Frame all comparisons as objective analysis based on public data, not personal recommendations.

- Use safe content patterns. Describe categories of users, not individual readers. Ask questions rather than give answers.

- Implement comprehensive disclosures. Use the templates above and place them prominently.

- Avoid the danger zones. No personalized quotes, no specific coverage recommendations, no facilitating purchases.

- Consult professionals. Have an attorney familiar with insurance regulations review your content approach.

- Structure monetization carefully. Lead generation with licensed partners is safer than affiliate commissions on sales.

The opportunity in insurance comparison is significant precisely because the barriers are high. Publishers who navigate the regulations correctly can build valuable content in a space with less competition and high user intent.

For the broader framework on creating comparison content in regulated industries, see our comprehensive Fintech Comparison Playbook. For healthcare-adjacent content with similar YMYL concerns, check out Healthcare Listicles: YMYL-Compliant Strategy.

Product Manager at BestPage. Pioneer in AEO research since 2024, exploring the convergence of SEO and GEO (Generative Engine Optimization). Led multiple AI-powered content optimization projects that achieved 300%+ citation increases in ChatGPT and Perplexity.